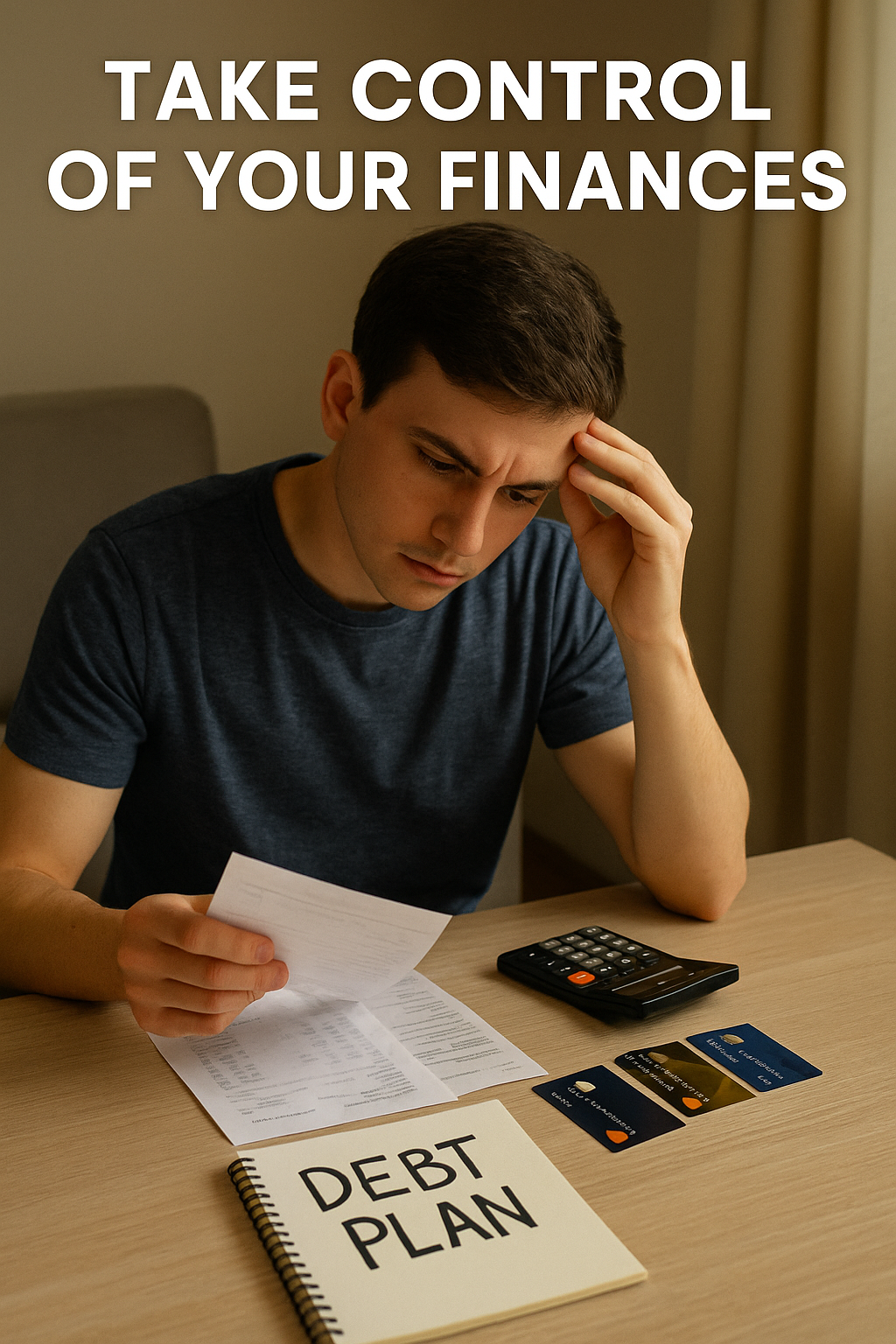

📉 Overwhelmed by Debt? You’re Not Alone.

Carrying $10,000 to $25,000 in debt in your 20s or 30s can feel like being buried alive—slowly suffocating under credit cards, student loans, or personal loans. You’re working hard, maybe juggling a side hustle, and yet the numbers just won’t go down.

That’s where debt consolidation can be a game-changer—it helps simplify your repayments and puts you back in control of your financial life.

But here’s the truth: you can absolutely take control, and debt consolidation might be your way out.

In this article, we’ll walk you through what debt consolidation really means, how it works, and the best ways to consolidate $10K–$25K in debt—without making things worse.

📌 What Is Debt Consolidation, Really?

Debt consolidation means combining multiple debts—like credit cards, student loans, or payday loans—into one monthly payment with a lower interest rate. It simplifies your life and can help you pay off your debt faster and cheaper.

Think of it like this: instead of juggling five balls (different debts), you’re now holding just one.

🔑 Best Ways to Consolidate $10K–$25K in Debt

✅ 1. Personal Debt Consolidation Loan

Apply for a personal loan from a trusted bank or online lender. If you have a fair credit score (650+), you could qualify for lower interest than your current debt.

Check top lenders here

✅ 2. Balance Transfer Credit Card

Use a 0% APR balance transfer card to transfer high-interest credit card balances. Pay off within the promo period (12–18 months).

✅ 3. Debt Management Plan (DMP)

Partner with a non-profit credit counseling agency to negotiate lower interest and create a structured repayment plan.

✅ 4. Use a Peer-to-Peer Lending Platform

Try platforms like Upstart or LendingClub if you have fair credit but want better loan terms.

✅ 5. Refinance Student Loans

If student loans are your main issue, refinancing could lower your interest rate significantly.

🧠 Is Debt Consolidation Right for You?

Before jumping in, ask yourself:

- Is my credit score strong enough to get lower interest?

- Can I commit to a single monthly payment?

- Will I stop adding new debt while paying this off?

If yes, debt consolidation can be life-changing. But if you tend to overspend or have unstable income, it may not be your best option unless you also change your habits.

💡 Pro Tips to Stay Debt-Free After Consolidation

- Automate your payments to avoid missing them.

- Don’t close old credit cards (they help your credit score).

- Build a small emergency fund—start with $500.

- Use budgeting apps like YNAB or Mint.

💬 Real Talk: My $22K Debt Journey

At 27, I had over $22,000 in debt—credit cards, student loans, everything. I took a personal loan to consolidate it. One payment. No juggling. Two years later, I was debt-free.

The peace of mind? Worth every hard decision.

🧾 Final Thought: Take the First Step

You don’t have to live with constant debt stress. Whether it’s a personal loan, balance transfer, or DMP—take the step that fits your life.

Even small actions make a big difference. Learn more from trusted sources like:

🏁 Why Consolidating Debt Is More Than Just a Financial Move

Taking control of your debt isn’t just about numbers—it’s about mental peace, freedom, and confidence in your future. You don’t have to be perfect or rich to fix your finances.

You just need a clear plan and the courage to begin. Debt consolidation is not a shortcut, but it’s a smart reset button many in their 20s and 30s desperately need.

Enjoyed this post?

Don’t keep it to yourself—share it with a friend who’s drowning in debt. You could change their life too.

Also read:

1 thought on “💥Debt Consolidation Dilemma: How People in Their 20s & 30s Can Escape $10K–$25K Debt Quickly and Fearlessly”